| Ticker: VOW | Nature of Business: Automaker | Location: Germany |

| Recent Price: €91.45 | 52-Week High/Low: €110.20/85.05 | Estimated Fair Value:€164.02 – €195.34 |

| Expected Return: 38.2% | Consider Buy: Below €164.02 | Business Risk: High |

| Financial Risk: Medium | Economic Moat: Weak | Corporate Governance: Strong |

Company Overview

VOLKSWAGEN is a German multinational automaker with over 100 production facilities in 26 countries in Europe, North America, South America, Asia and Africa. The company was established in 1937 by the German Labour Front, a national trade union, to produce affordable and accessible cars for the masses. After the outbreak of World War II in 1939, the company experienced a shift in focus from the production of civilian cars to the production of military goods and weapons. The production of its first non-military car, the Beetle, started in 1945.

VOLKSWAGEN has three major shareholders at the end of the 2025 fiscal year, namely Porsche Automobil Holding SE (PAH), Qatar Holding LLC (QH) and the State of Lower Saxony (SLS). PAH, which holds 31.9% of the company’s subscribed capital, has 53.3% of the voting rights. QH and SLS, with 10.4% and 11.8% of the subscribed capital respectively, have 17% and 20% of the voting rights respectively. The company’s shares have been trading on the Frankfurt Stock Exchange since 1961.

Technological innovation, strategic partnership and streamlined operations are central to the company’s transition from the manufacture of conventional internal combustion vehicles to sustainable energy vehicles. Its product portfolio now includes all-electric and hybrid vehicles, which are produced to meet the different requirements of customers.

Oliver Blume was named chairman of the 8-member Board of Management of VOLKSWAGEN in 2022. Blume, who rose through the ranks, became chairman after about 3 decades with the company. The supervisory board is a 20-member board that keeps an eye on the company’s management and appoints the members of the Board of Management. The supervisory board is chaired by Hans Dieter Pötsch, who brings his extensive experience in the automotive industry to bear on the company.

Investment Thesis

VOLKSWAGEN has widely recognised brands such as Volkswagen, Skoda, Audi, Bentley, Lamborghini and Porsche. The company, which started as a traditional car maker, is pushing boundaries through its artificial intelligence and advanced driver assistance systems. It is investing significantly in research and development and strategic partnerships. The demand for the company’s electric vehicles is rising; the deliveries of its all-electric vehicles rose by 32% in 2025. In addition, 10.9% of car deliveries were all-electric vehicles (2024:8.2%).

The company is not resting on its oars. It is strengthening its product portfolio by adding models of its vehicles with improved design and quality. In 2025 alone, it launched about 30 new models and more models are in the pipeline. These new models are expected to improve both its top-line and bottom-line going forward.

The company operates on thin profit margins owing to the high cost of sales. On the whole, the cost of sales to turnover ratio stands at 81.5% while the gross profit margin averages out to 18.5%. The 10-year average operating profit margin stood at 5.8%. The management, as a result, is streamlining operations and investing in technology for the purpose of cutting costs and improving profit margins. We expect those efforts to pay off going forward. For example, VOLKSWAGEN is poised to benefit from cost savings and improved quality control from the production of its own batteries through one of its subsidiaries, PowerCo SE. It will cease to rely completely on external battery suppliers as soon as PowerCo becomes fully operational.

Sales growth in Asia and North America has stalled in recent years. Revenue from Asia/Pacific region decreased for three consecutive years, while it has been on the downhill for two straight years in North America. Together, Asia/Pacific and North America have generated, on average, 35.1% of VOLKSWAGEN’s total revenue. The European market remains a key revenue stronghold for VOLKSWAGEN. Europe has been responsible for the bulk of its revenue, producing about 60% of its total revenue over the past 10 years.

The efforts of the management to improve consumer preference for its brands in China and the US are commendable. It is leveraging its collaborations for enhanced functionalities of its electric vehicles. The company has partnered with Rivian Automotive, Inc. (USA) to develop advanced vehicle technology for its electric vehicles from 2027. In addition, its technical collaboration with Xpeng in China will facilitate the production of all-electric, plug-in hybrid and range-extended models in that country; this should boost sales amid the rising competitive pressure in China.

VOLKSWAGEN remains a profitable company. It is Europe’s largest car maker. Even though the company pays dividends regularly, it has relied more on debt than shareholders’ equity to finance its operations. But it has consistently generated enough operating profit and operating cash flow to pay its interests.

Valuation

VOLKSWAGEN is currently trading at a hefty discount to our fair value estimate, ranging from €164.02 to €195.34 per share. Expected return on the company’s stock is 38.2%.

Financial Overview

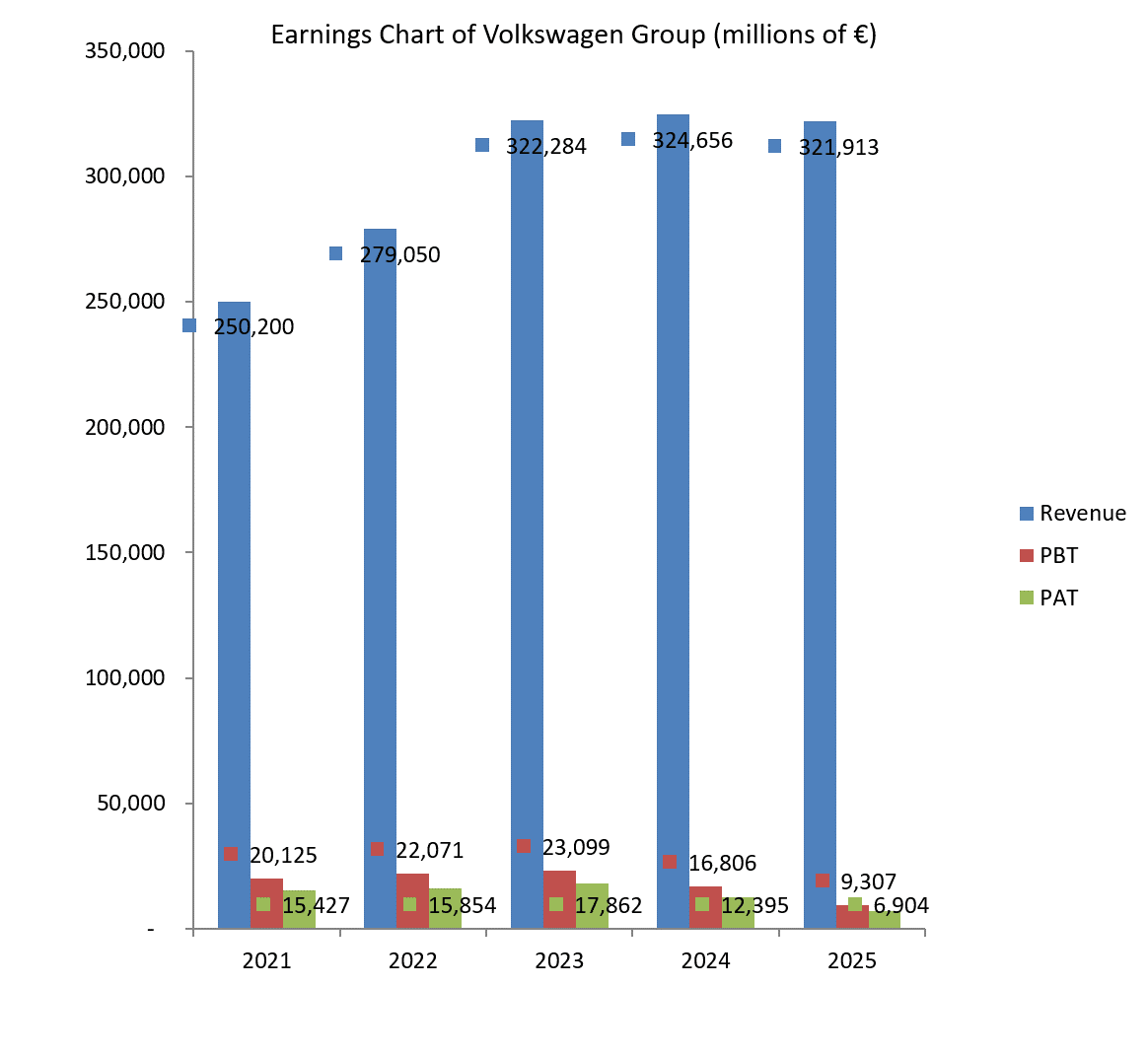

VOLKSWAGEN’s revenue was more or less flat at €321.9 billion in 2025, owing to the sales drop in its North America and Asia/Pacific markets. Revenue from Europe and other markets (including Germany), which increased from €194.1 billion in 2024 to €204.5 billion in 2025, amounted to a 5.4% year-on-year growth. Sales revenue in North America shed €7.7 billion or 11.4% year-on-year, while Asia/Pacific’s revenue of €38.2 billion in 2025 represented a 13.4% decline. Sales from South America were more or less flat at €19 billion.

The company has three operating segments, namely Passenger Cars and Light Commercial Vehicles segment, Commercial Vehicles segment and Financial Services segment. Revenue from Passenger Cars and Light Commercial Vehicles grew by 1.2% in 2025, as against a 1.7% decline in the previous year. Commercial vehicles lost 7.9% of the previous year’s revenue, while the Financial Services segment experienced a 5.7% year-on-year revenue increase. But it is worthy of note that the Passenger Cars and Light Commercial Vehicles segment remains its major source of revenue, accounting for about 70% of its total sales revenue.

A 2.1% rise in cost of sales resulted in a 13.8% fall in gross profit from €59.5 billion in 2024 to €51.2 billion in 2025. Gross profit margin lost 2.4 percentage points to close at 15.9% at the end of the 2025 fiscal year. The company posted an operating profit of €8.9 billion in 2025, as against €19.1 billion in the previous year. A 53.5% year-on-year decrease in operating profit caused the operating profit margin to drop to 2.8% compared to the prior year’s 5.9%. Profit Before Tax (PBT) was €9.3 billion in 2025, down by 44.6% from €16.8 billion in 2024. Likewise, Profit After Tax (PAT) shed 44.3% to €6.9 billion.

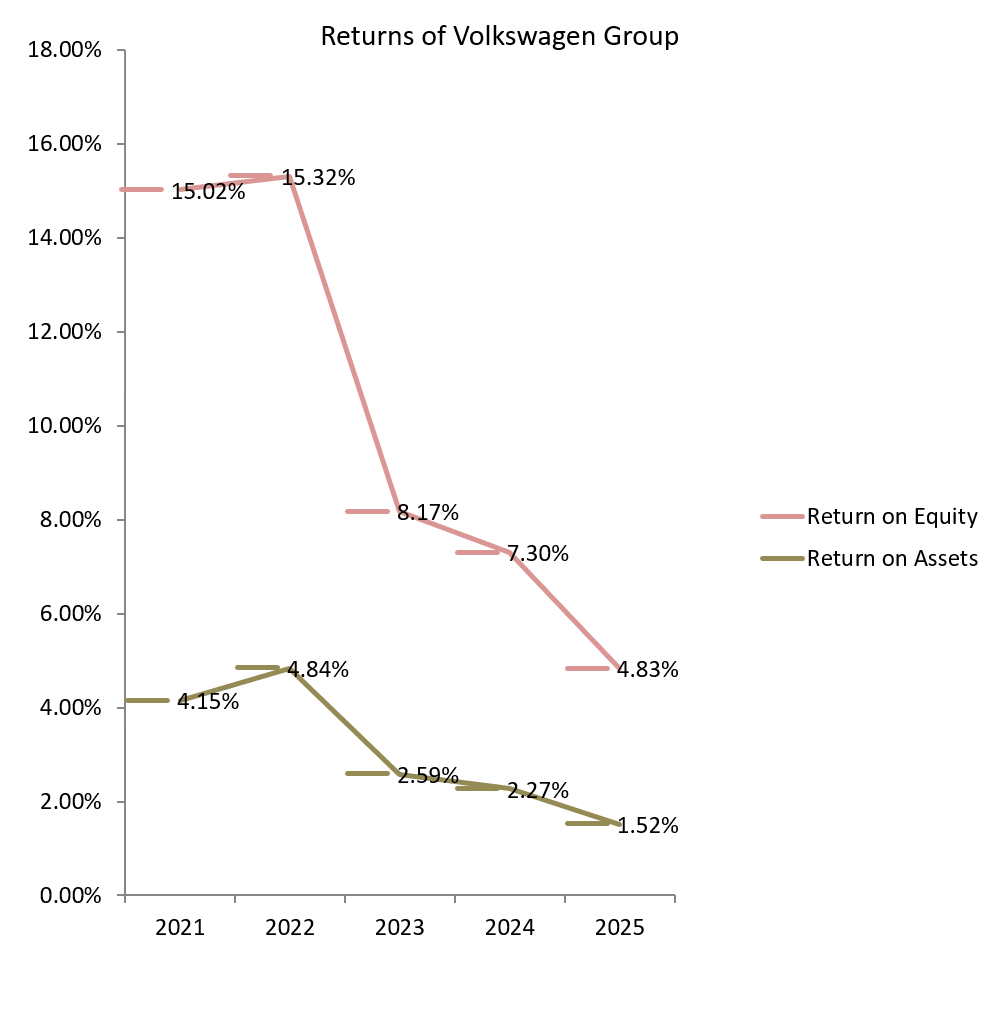

The total assets of €644.5 billion and total equity of €203.1 billion have grown at a compound annual rate of 4.5% and 4.4% respectively, over the past three years. Both Return on Equity (RoE) and Return on Assets (RoA) decreased from 7.3% and 2.3% respectively, in 2024 to 4.8% and 1.5% in 2025. Total debt stood at €264.7 billion (2024: €254.1 billion). Though total debt accounted for close to 40% of total assets, it has always exceeded the total equity. We, however, do not have any cause to believe that VOLKSWAGEN is insolvent or that its financial viability is impaired.

Business Risk

Although VOLKSWAGEN has become a powerhouse in the European electric vehicle market, it is still facing competition, especially from cheaper Chinese electric vehicle manufacturers that are penetrating the European market. Its ability to drive down its costs and achieve technological superiority will be important in warding off competitors in Europe and beyond.

Recommendation: Buy

| (€ in Million) | 2025 | 2024 | 2023 | 2022 | 2021 |

| Turnover | 321,913 | 324,656 | 322,284 | 279,050 | 250,200 |

| Year-on-Year Change | -0.8% | 0.7% | 15.5% | 11.5% | 12.3% |

| Operating Profit | 8,868 | 19,060 | 22,529 | 22,110 | 19,275 |

| Year-on-Year Change | -53.5% | -15.4% | 1.9% | 14.7% | 99.2% |

| EBITDA | 46,340 | 51,116 | 34,256 | 35,474 | 32,222 |

| Year-on-Year Change | -9.3% | 49.2% | -3.4% | 10.1% | 43.6% |

| PBT | 9,307 | 16,806 | 23,099 | 22,071 | 20,125 |

| Year-on-Year Change | -44.6% | -27.2% | 4.7% | 9.7% | 72.5% |

| PAT | 6,904 | 12,395 | 17,862 | 15,854 | 15,427 |

| Year-on-Year Change | -44.3% | -30.6% | 12.7% | 2.8% | 74.9% |

| Total Assets | 644,466 | 632,905 | 600,338 | 564,015 | 528,610 |

| Year-on-Year Change | 1.8% | 5.4% | 6.4% | 6.7% | 6.3% |

| Net Current Assets | 21,339 | 28,192 | 33,768 | 41,437 | 35,955 |

| Year-on-Year Change | -24.3% | -16.5% | -18.5% | 15.3% | 21.8% |

| Total Equity | 203,053 | 196,731 | 189,912 | 178,328 | 146,153 |

| Year-on-Year Change | 3.2% | 3.6% | 6.5% | 22.0% | 13.5% |

| Capital Expenditure | 26,811 | 29,882 | 28,511 | 26,297 | 24,397 |

| Year-on-Year Change | -10.3% | 4.8% | 8.4% | 7.8% | 25.9% |

| Funds from Operations | 15,009 | 17,151 | 19,356 | 28,496 | 38,633 |

| Year-on-Year Change | -12.5% | -11.4% | -32.1% | -26.2% | 55.2% |

| Free Operating Cashflow | -11,802 | -12,731 | -9,155 | 2,199 | 14,236 |

| Year-on-Year Change | -7.3% | 39.1% | -516.3% | -84.6% | 157.9% |

| Total Debt | 264,703 | 254,081 | 232,799 | 205,185 | 210,202 |

| Year-on-Year Change | 4.2% | 9.1% | 13.5% | -2.4% | 3.3% |

| Net Debt | 225,902 | 213,785 | 189,350 | 176,013 | 170,479 |

| Year-on-Year Change | 5.7% | 12.9% | 7.6% | 3.3% | 0.6% |

| Shares Outstanding-ordinary shares (Million) | 295 | 295 | 295 | 295 | 295 |

| Year-on-Year Change | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

| Payout Ratio | 39.1% | 29.5% | 28.2% | 29.3% | 25.4% |

| ⇑ – Year-on-Year Increase | Green: ‘Improved’ |

| ⇓ – Year-on-Year Decrease | Red: ‘Worsened’ |

| ⇔ – Year-on-Year Unchanged |

| 2025 | 2024 | 2023 | 2022 | 2021 | |

| CAPITAL STRUCTURE | |||||

| Total Debt/(Total Debt + Equity) | 56.6%⇑ | 56.4%⇑ | 55.1%⇑ | 53.5%⇓ | 59.0%⇓ |

| Net Debt/Equity | 111.3%⇑ | 108.7%⇑ | 99.7%⇑ | 98.7%⇓ | 116.6%⇓ |

| Debt/Total Assets | 41.1%⇑ | 40.2%⇑ | 38.8%⇑ | 36.4%⇓ | 39.8%⇓ |

| Long Term Debt/Net Earnings | 14.0x⇑ | 9.5x⇑ | 7.9x⇑ | 4.5x⇓ | 6.0x⇓ |

| Current Ratio | 1.1x⇔ | 1.1x⇓ | 1.2x⇔ | 1.2x⇔ | 1.2x⇔ |

| Acid Test Ratio | 0.9x⇔ | 0.9x⇔ | 0.9x⇔ | 0.9x⇓ | 1.0x⇑ |

| CASHFLOW RATIOS | |||||

| Funds from Operations/Total Debt | 0.1x⇔ | 0.1x⇔ | 0.1x⇔ | 0.1x⇓ | 0.2x⇑ |

| Funds from Operations/Net Debt | 0.1x⇔ | 0.1x⇔ | 0.1x⇓ | 0.2x⇔ | 0.2x⇔ |

| EBITDA/Interest | 14.3x⇓ | 14.8x⇑ | 9.4x⇓ | 87.0x⇑ | 17.7x⇑ |

| EBIT/Interest | 2.7x⇓ | 5.5x⇓ | 6.2x⇓ | 54.2x⇑ | 10.6x⇑ |

| Net Debt/EBITDA | 4.9x⇑ | 4.2x⇓ | 5.5x⇑ | 5.0x⇓ | 5.3x⇓ |

| Free Operating Cashflow/Interest | -3.6x⇑ | -3.7x⇓ | -2.5x⇓ | 5.4x⇓ | 7.8x⇑ |

| Free Operating Cashflow/Net Debt | -0.1x⇔ | -0.1x⇔ | -0.1x⇓ | 0.0x⇓ | 0.1x⇑ |

| Free Operating Cashflow/Sales | 0.0x⇔ | 0.0x⇔ | 0.0x⇔ | 0.0x⇓ | 0.1x⇑ |

| PROFITABILITY RATIOS | |||||

| Gross Profit Margin | 15.9%⇓ | 18.3%⇓ | 18.9%⇑ | 18.7%⇓ | 18.9%⇑ |

| EBITDA Margin | 14.4%⇑ | 15.7%⇑ | 10.6%⇓ | 12.7%⇓ | 12.9%⇑ |

| EBIT Margin | 2.8%⇓ | 5.9%⇓ | 7.0%⇓ | 7.9%⇑ | 7.7%⇑ |

| PBT Margin | 2.9%⇓ | 5.2%⇓ | 7.2%⇓ | 7.9%⇓ | 8.0%⇑ |

| PAT Margin | 2.1%⇓ | 3.8%⇓ | 5.5%⇓ | 5.7%⇓ | 6.2%⇑ |

| ROAE | 4.9%⇓ | 7.4%⇓ | 8.4%⇓ | 16.8%⇑ | 16.0%⇑ |

| ROAA | 1.5%⇓ | 2.3%⇓ | 2.7%⇓ | 5.0%⇑ | 4.3%⇑ |